So what’s the future of finance? Is decentralized finance better than the current financial system? What problems does it solve? And does it have a chance to improve or completely replace traditional finance? You’ll find answers to these questions in this article.

The Financial System

The financial system that we know today went through decades of technological advances.

The earliest attempts to make finance more efficient started as early as the 1920s with the introduction of accounting machines and punch cards. This was followed by the rise of the mainframe computers that significantly sped up the banking system in the 1950s and beyond.

The next revolution was the invention of ATMs and credit cards that started being popular in the 1970s. Also in the 1970s, another important element of the financial system, the stock market, started going through a radical transformation. Manual order entries and loud trading pits started being slowly replaced by computers and algorithms.

From the 1990s, thanks to the growing adoption of the Internet, the computerization of finance got supercharged. Accessing bank accounts, making wire transfers, buying stocks, all of these operations were now possible from the comfort of our own houses.

Then comes the fintech revolution. PayPal, Robinhood, TransferWise, Revolut and other fintech startups understood the tech-first approach known from other non-financial tech companies and offered their users seamless access to financial services – a completely different experience when compared to the clunky banking user interfaces.

Despite a century of innovations, the financial system is far from being perfect.

Settlement of stocks, bonds and other financial instruments takes days to clear and requires a massive amount of human capital involved in the process.

Key decisions impacting millions if not billions of people are made behind the closed doors by a group of privileged few.

Billion-dollar banking scandals that surface months if not years after the fact.

Massive inefficiencies and high cost when it comes to international banking and remittance services.

Unequal access to financial services with billions of unbanked people across the globe.

Banks hiring thousands of employees just to keep maintaining inefficient processes and being compliant with ever-changing banking regulations.

A super high barrier to entry for the new players making it almost impossible to start a new financial company without access to the massive amount of capital, stifling innovation.

The whole financial infrastructure consists of siloed systems built with proprietary technologies and algorithms that each company has to make from scratch.

The beautiful user interfaces provided by fintech companies only cover the fact that the financial system is built on old and inefficient foundations. Something that seems to be instant for the user can take days to fully process behind the scene.

On top of that, the backbone of the financial system hasn’t evolved much since the mainframe computers were introduced. This is exactly why we need something new, something better, that can address some of these problems.

And this is where decentralized finance comes into play.

DeFi

Instead of relying on old and inefficient infrastructure, Decentralized finance, or DeFi, leverages the power of cryptography, decentralization and blockchain to build a new financial system.

A system that can provide access to well-known financial services such as payments, lending, borrowing and trading in a more efficient, fair and open way.

Efficient – as all operations are settled almost immediately. It doesn’t matter that counterparties may be in completely different geographic locations with inconsistent laws and regulations. On top of this, most of DeFi protocols can operate with no or minimal human involvement.

Fair – as all services are completely permissionless and censorship-resistant.

Permissionless – as everyone with a browser and the Internet connection can access them. There is no document verification, no need to provide income statements, nationality or race doesn’t matter – everyone is treated in the exact same way.

Censorship-resistant – as no other parties can deny us access to these services. Even multiple bad actors cannot change the rules of a sufficiently decentralized system.

Open – as everyone can build a new defi application and contribute to the ecosystem. In contrast to traditional finance, new applications can leverage the existing protocols and build on top of existing solutions.

On top of that, everything is transparent and visible on the blockchain. Trading volume, number of outstanding loans, total debt? All of these can be reliably checked on the blockchain. Even better, these numbers cannot be tampered with.

All of this is possible thanks to the invention of Bitcoin and Ethereum and their underlying technologies. In particular, Ethereum as a smart contract platform allows for creating any arbitrary financial applications. Because of these characteristics, Ethereum became a go-to blockchain for the vast majority of DeFi activities.

Decentralized finance has recently been experiencing tremendous growth.

Some of the key metrics are:

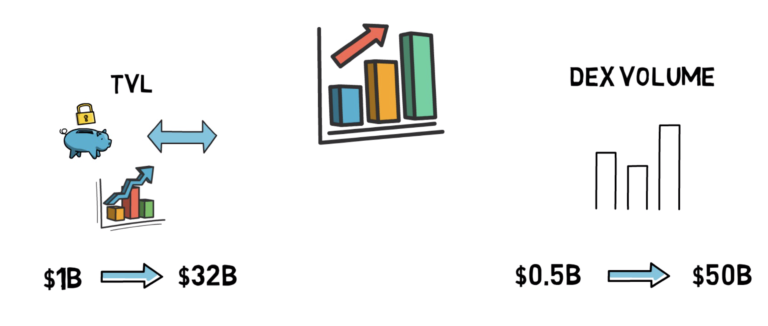

Total Value Locked in DeFi – this represents the value of all tokens locked in various defi protocols such as lending platforms, decentralized exchanges or derivatives protocols.

This number has grown from less than $1B in April 2020 to over $32B in February 2021.

Another important metric is the trading volume across decentralized exchanges.

This figure has grown from around $0.5B in April 2020 to over $50B in January 2021 – a 100x increase.

Total value settled on Ethereum has reached over $1T in 2020. This is more than PayPal.

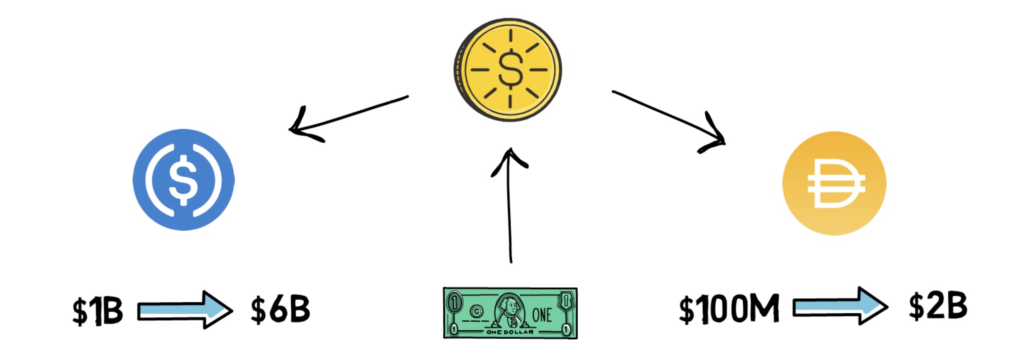

And all of this is not only limited to cryptocurrencies that, as we know, can be quite volatile in nature. Stable coins that track the value of fiat currencies, such as the US Dollar, also experienced tremendous growth in the DeFi ecosystem.

The market cap of USDC – a popular stable coin in DeFi – went from less than $1B in April 2020 to over $6B in 2021. Another one – DAI – went from less than $100M in April 2020 to almost $2B in 2021.

Problems in traditional finance

Now, to understand the value proposition of decentralized finance even better, let’s go through a few common problems in traditional finance and see how they can be addressed in DeFi.

Let’s start with a recent situation in the stock market – the famous Gamestop saga.

After discovering that Gamestop stock – GME – was overly shorted by some of the hedge funds, users of a popular Reddit group – Wall Street Bets – started buying GME as they believed this could initiate a short squeeze that would result in hedge funds having to buy back the shorted stock, driving the price higher.

At some point, Robinhood and a few other stock brokers came up with a controversial decision to disable the possibility of selling GME and a few other stocks.

A situation like this just wouldn’t be possible on a decentralized exchange like Uniswap.

There is no one who can disable or alter the trading capabilities of the platform. There is no single authority making decisions on behalf of the users. DeFi democratizes access to trading.

This situation exposes another problem – decisions made behind closed doors.

A group of people deciding to shut down trading? Or maybe a bunch of bankers deciding what the best interest rate is for millions of people?

In DeFi, interest rates are adjusted automatically based on the supply, demand and risk parameters of certain assets that are configured by the protocol.

Even if some DeFi lending platforms allow for changing certain risk parameters, all decisions are publicly visible and changes are voted on by multiple people who govern the protocol.

What about this problem – paying 10-30% of the value of a bank transfer just to send money across the globe? In DeFi, you can send USD-based stable coins for a fraction of that cost. Even better, they will arrive in a matter of seconds.

With the settlement of different assets measured in seconds instead of days, the counterparty risk is dramatically reduced.

Accounting? Every record is publicly available on the blockchain, so accounting becomes super easy and can be most likely completely automated. This can dramatically reduce the human capital needed.

Unequal access to financial services? A DeFi protocol doesn’t care who you are – it just follows predefined rules that are exactly the same for everybody.

Although DeFi presents us with a unique value proposition, it comes with its own challenges.

Challenges

It brings more responsibility to the users who are now truly owning their assets, so they have to make sure they store them in a secure way. There is not a lot of hand-holding here, especially when interacting with new DeFi protocols.

There are still certain regulatory risks. Although things like KYC or AML cannot be enforced in the DeFi protocols themselves, the regulator may try to force wallet providers or dev teams responsible for certain protocols to add KYC requirements to their user interfaces.

Scaling is another issue that has to be tackled. The popularity of DeFi resulted in a tremendous demand for the block space on Ethereum. This in turn results in high gas fees for the users. It’s not uncommon to hear about $10 or even $50 Uniswap transaction costs.

Scaling is already being tackled by Eth2 and Layer2 scaling solutions. You can learn more about it here.

Hacks are another challenge of the DeFi space that make using certain protocols, especially the new ones risky.

Various DeFi protocols are also exploring different governance models, however, whales and voter’s apathy are some of the common problems here.

Uncollateralized loans and mortgages are big areas of traditional finance that are slightly harder to implement in DeFi. Fortunately enough, there are already protocols like Aave exploring different possibilities such as credit delegation and tokenized mortgages.

Despite the challenges, DeFi is a unique innovation, a 0 to 1 innovation. And I believe that sorting out some of these challenges is just a matter of time.

Summary

So what will happen to traditional finance if DeFi keeps innovating and growing at this tremendous pace?

Personally, I think that traditional finance will have to adapt quickly, otherwise, they are taking a risk of slowly becoming irrelevant. Like with all other big technological changes, they often happen gradually, then suddenly.

We’ll probably very quickly see some of the incumbents trying to tap into the possibilities of DeFi. For example, by leveraging liquidity or accessing more favourable interest rates in one of the DeFi protocols. This will most likely start with fintech companies that are already involved in crypto but I wouldn’t be surprised to see banks using DeFi in a few years time.

There are also a lot of areas of traditional finance that can significantly benefit from moving into DeFi in the future. As an example, instead of going public on the stock market, companies could issue security tokens and take advantage of globally accessible liquidity. On top of this, people investing in these tokens could lend them out and make an extra yield on their investment or use them as collateral for taking a loan.

It’s also very likely that DeFi will become a new backbone of the financial system. With simple user interfaces, most people will probably not even know they’re using it, in similarity to how they don’t know what is happening under the hood of their traditional trading application. At this point, DeFi will just become finance. More efficient, fair and open finance.

So what do you think about the future of finance? How big will DeFi become?

If you enjoyed reading this article you can also check out Finematics on Youtube and Twitter.